Results of Aviation Business Strategies Group’s (ABSG) Annual FBO Fuel Sales Survey indicates that fuel sales softened in 2023 following a relatively lackluster 2022 performance.

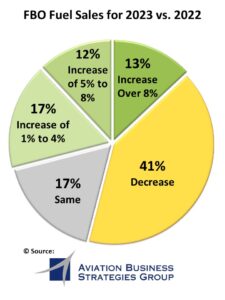

According to ABSGs Principals John Enticknap and Ron Jackson, the overall survey results showed an unusually high number of FBOs, 41 percent, reporting a decrease in fuel sales in 2023 compared to 2022.

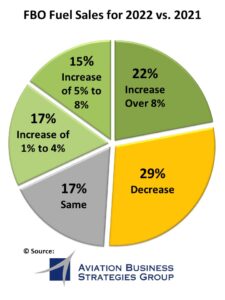

By comparison, 29 percent of survey respondents reported a decline in fuel sales in 2022 vs. 2021, a differential of 12 percent.

In addition, two other response categories underperformed in 2023 compared to 2022 with the percentage of FBOs reporting increased fuel sales of at least five percent to more than eight percent skewed lower than the 2022 survey results. (Refer to graphs.)

“After FBO fuel sales recovered in 2021 to pre-pandemic levels, we have seen a gradual softening across the market spectrum over the past two years,” Enticknap said. “This downward trend seems to indicate that the General Aviation market is testing a lower annual fuel volume level as Jet A fuel prices remain mostly elevated.”

Jackson said the that survey respondents indicated several factors that contributed to the softening in fuel sales.

“The underlying contributing factors reported in the survey included increased inflationary pressures, elevated cost of Jet A and higher interest rates which hindered corporate borrowing, all of which impacted flight department budgets,” Jackson explained. “Further acerbating the situation was a continuing downturn in Part 135 flights which appears to be an aftershock effect from high charter demand during the peak of the pandemic.”

contributing factors reported in the survey included increased inflationary pressures, elevated cost of Jet A and higher interest rates which hindered corporate borrowing, all of which impacted flight department budgets,” Jackson explained. “Further acerbating the situation was a continuing downturn in Part 135 flights which appears to be an aftershock effect from high charter demand during the peak of the pandemic.”

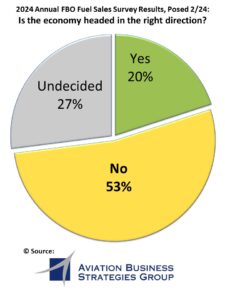

Confidence in the Economy

According to ABSG, confidence in the economy remained low as 53% of the survey respondents said the economy is headed in the wrong direction with only 20% providing a positive response while 27% were undecided.

Top 5 FBO Industry Concerns

Another area the ABSG survey explores with FBO operators involves feedback regarding their concerns and greatest challenges facing the industry. An open-ended question resulted in these top five concerns:

- High cost of constructing new hangars: FBOs are facing elevated construction costs and higher bank loan rates causing a slowdown in expansion of needed infrastructure. Increased construction costs have been estimated to be as much as 30 percent higher from prices recorded in 2021.

- Effects of inflation/higher cost of doing business:

- Higher overhead costs to include labor, goods, services, insurance, facility upkeep and utilities.

- Airport authorities raising operating fees; more restrictive government regulatory oversight.

- Fear that smaller/family owned FBOs won’t be able to remain competitive.

- Replacing 100 LL with 100UL: FBOs are concerned about potential costs involved in switching over to unleaded Avgas to include tank farm/storage issues, fuel quality control, availability and the actual cost of the fuel. Many FBOs responding to the survey fear that the average piston aircraft owner/pilot will be priced out of aircraft ownership.

- Cost of GSE repair and replacement: More and more FBOs are facing higher costs to repair and/or replace GSE equipment.

- Finding and keeping qualified employees: This includes A&P technicians, the cost of training new employees and ongoing retention issues.

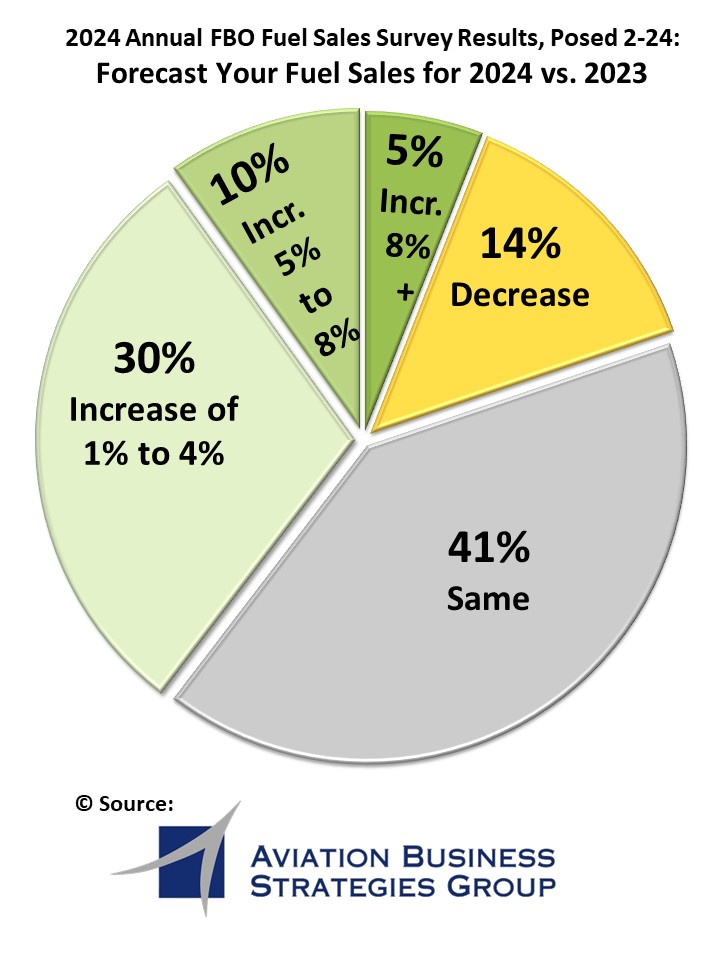

FBO Industry Forecast for 2024 and Beyond: Fuel Sales to Remain Flat

- Fuels Sales for 2024. (Refer to associated graph.)

ABSG asked survey respondents to forecast their fuel sales for 2024. The following is the cumulative data received:

- Same as 2023: 41 percent

- A decrease in fuel sales: 14 percent

- Increase of one to four percent: 30 percent

- Increase of five to eight percent: 10 percent

- Increase of more than eight percent: 5 percent

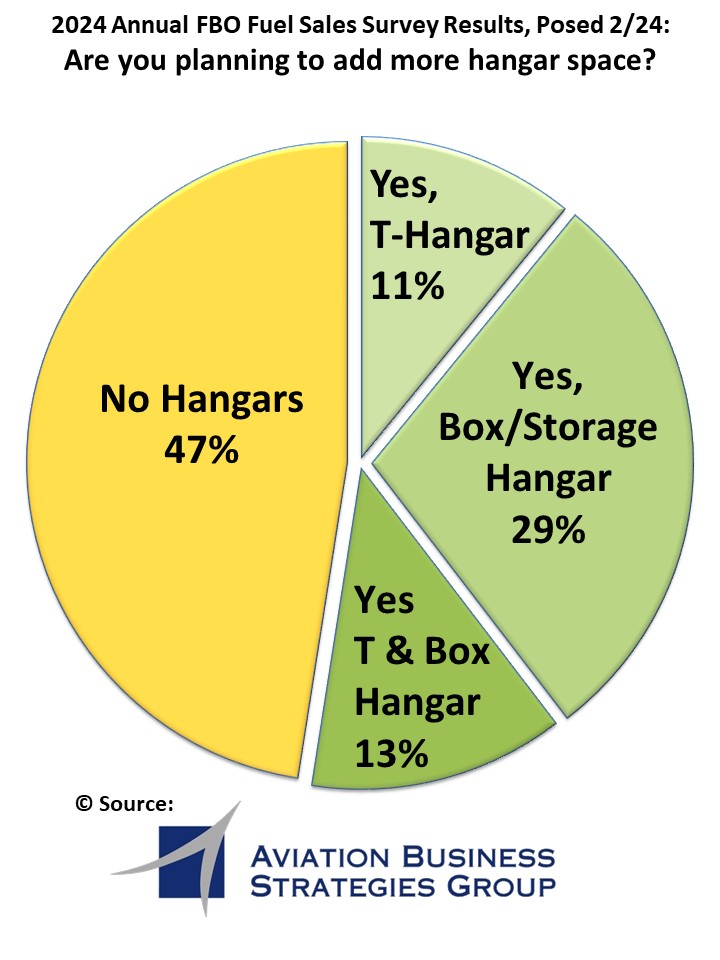

- Adding more hangar space. (Refer to associated graph.)

ABSG asked respondents if they were planning on adding more hangar space going forward. The following is their response:

- Yes, adding T-hangars: 11 percent

- Yes, adding box/storage hangar: 29 percent

- Yes, adding both T-hangars and box/storage hangars: 13 percent

- No, not adding any hangar space: 47 percent

- Economy/inflation.

Markets indicate a very slow decline in inflation in 2024 as the Federal Reserve tries to get nearer to their two percent goal.

- Interest Rates.

Expect no cuts in interest rates until there is consistent/positive economic data over at least two quarters for two primary price indexes: Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) index.

- Price of Oil/Jet A Fuel.

Oil prices have mostly settled between $70 and $80 per barrel for WTI causing Jet A prices to remain elevated from pre-pandemic levels. As the Presidential election inches closer in November, expect to see some easing of oil prices. However, pressure from ever-changing geo/political forces and events can cause moderate to large swings in pricing for the rest of the year. As in the past, the cost of Jet A will follow the cost of a barrel of oil.

- Business Aircraft Flight Activity.

According to Argus International in their 2023 Business Aviation Review, business aircraft flight activity in North America declined in 2023 compared to 2022. By segment, Part 91 flight activity dropped 2.6 percent, equivalent to 42,569 fewer flights, while Part 135 operations were down 8.6 percent year-over-year representing 121,551 less flights.

Expect business aircraft flight hours to keep flattening in 2024 and continue a moderating trend until inflation and the cost of crude oil are tamed.

- Prospects of Recession/Higher Unemployment.

As part of the Fed’s quest to quell inflation, the effects of higher interest rates over a longer period of time will eventually cause a softening in consumer spending and economic confidence, forcing businesses to trim labor costs. The potential for a rise in the unemployment rate will make it harder for the Fed to realize a soft economic landing. At some point, there will be a new normal that will dictate the health of the FBO industry for a period of at least 12 to 15 months.

- Cash is King.

FBOs should operate as if cash were king. Higher interest loans will continue to force FBOs to put off major improvements to infrastructure such as new hangars and terminal buildings. FBOs that are prepared to weather the next 12 months are those that watch their fuel margins closely. Keep steady and avoid deep fuel discounting to attract business.

By Aviation Business Strategies Group

Aviation Business Strategies Group (ABSG) was founded in 2006 by aviation services veterans John Enticknap and Ron Jackson.